Affordable housing was the top priority in BC Budget 2024 and the government plans to make significant capital commitments to get middle-income earners into market homes and provide more supports and protections for renters.

Here are the highlights for property buyers, renters, and small business.

Property Transfer Tax (PTT)

The first-time homebuyers’ exemption

Effective April 1, 2024, the threshold is increased from $500,000 to $835,000, with the first $500,000 exempt from property transfer tax. The phase out range is $25,000 above the threshold, with the complete elimination of the exemption at $860,000.

The newly built home exemption threshold

This threshold now eliminates the PTT for eligible first-time home buyers on new homes up to $1,100,000 from the previous $750,000. The phase out range is $50,000 above the threshold, with the complete elimination of the exemption at $1,150,000 for qualifying newly built homes.

New purpose-built rental buildings

Buyers of new qualifying purpose-built rental buildings will be exempt from the PTT starting January 1, 2025 and ending December 31, 2030. This exemption builds on the further two per cent property transfer tax exemption for new purpose-built rentals announced in Budget 2023 and the rental housing revitalization tax exemption provided in Budget 2018.

PTT exemptions dates

Increase threshold for first time home buyers’ exemption – begins April 1, 2024.

Increase threshold for newly built home exemption – begins April 1, 2024.

Enhanced exemption for new purpose-built rental buildings – begins January 1, 2025 and ends December 31, 2030.

The government estimates these new PTT exemption thresholds will save homebuyers about $8,000 and British Columbians over $100 million annually, and up to 14,500 homebuyers – twice as many as before – will now be eligible for the PTT exemption.

PTT revenue growth is expected to average 8.6 per cent annually over the next two years.

Note: For more than two decades, Greater Vancouver REALTORS® have been advocating for changes to the PTT, meeting with politicians and providing submissions each year. Government has finally listened.

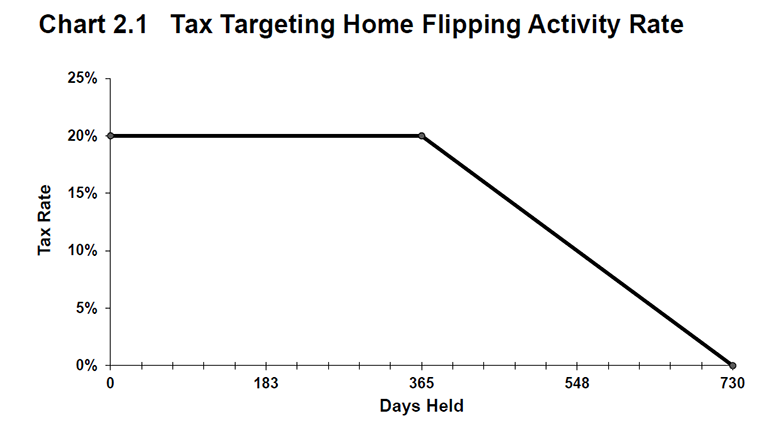

Flipping tax

The government is bringing in a new flipping tax, effective January 1, 2025, on the profit made from selling a residential property, including a presale assignment, within two years of buying it.

The rate is 20 per cent within the first year of purchase, declining to zero between 366 and 730 days. The tax will not apply to land or portions of land used for non-residential purposes.

There are exemptions for

those adding to the supply of housing or engaging in real estate development and construction

life circumstances including separation or divorce, death, disability or illness, relocation for work, involuntary job loss, a change in household membership, personal safety, or insolvency

In addition to these exemptions, individuals selling their primary residence within two years of purchase can exclude a maximum of $20,000 when calculating their taxable income.

The government estimates the tax would generate $44 million in revenue in the 2025/2026 fiscal year, which is slated for affordable housing.

Source: BC Budget 2024, page 66.

BC Builds and supporting renters

BC Builds, launched in February 2024, includes $198 million over three years and leverages government-owned, public, and underused land, and low-cost financing to bring down construction costs and deliver more middle-class rental and market housing.

Secondary suites

Forgivable loans up to $40,000 for homeowners to build and rent secondary suites below market rates to quickly increase affordable rental supply.

Renter tax credit

An annual income-tested tax credit of up to $400 per year for renters.

Zoning and permitting

Allowing small-scale, multi-unit affordable housing including townhomes, duplexes, and triplexes through zoning changes and proactive partnerships.

Streamlining permitting to reduce costs and speed up approvals to get homes built faster.

Short-term rentals

Strengthening enforcement of short-term rental regulation.

Electricity tax credit

A new, one year electricity affordability credit for all households, regardless of income starting in April 2024. Households will save on average $100 a year on their electricity bills.

Commercial and industrial customers will receive savings of about 4.6 per cent based or about $400 on their 2023/24 electricity bills.

Climate change and climate action

More than $1 billion in new spending measures to help protect British Columbians from the effects of climate change and build a greener economy.

The Climate Action Tax Credit increases to $1,005 per year for families up to four persons, up from $890 last year. Individuals will receive $504 compared to $447 last year. Start date is in July 2024.

Small business

There is $100 million in relief for the employer health tax, including the continuation of the venture capital tax credit, and the expansion of the interactive digital media tax credit.

Deficit and debt

The government estimates this years’ deficit at $5.914 billion rising to $7.773 billion by 2026.

The total debt will rise from $103 billion to $123 billion in 2024-25.

More information

Read the BC Government news release on BC Budget 2024.

Read Budget BC 2024 Highlights regarding housing.

Read the BC 2024 Budget speech.

Visit the BC Budget 2024 website.

Read BC Budget 2024 (opens a 170-page pdf).

If you have questions about the BC Budget, contact Harriet Permut, director of government relations at hpermut@gvrealtors.ca